Home buyers guide

Buying your first home is a huge achievement. However, we know it can also feel overwhelming. Knowing what to do and when to do it, what happens next in the process, or even just how to get started. Whether you’re ready to buy your first home now or just starting to think about, doing your research and being well-informed is key to helping you feel ready for making the decision to get a home loan.

In this guide, we run through the key things you’ll need to know about buying a home in New Zealand from start to finish.

Where to start?

Saving for your deposit

When you’re ready to buy your home, the price you pay typically a combination of two parts:

Your deposit and a home loan (aka mortgage). You’ll need to sort both your deposit and home loan when it comes to the buying process.

- Your deposit

This is the upfront cash you’ll need to pay when you first buy your home. Typically, home loan lenders in New Zealand will require 20% of the property’s purchase price. However, this can vary across different lenders and personal situations

When you go unconditional on a house (when all conditions in the sale are met), a portion of your deposit is paid to the seller. So, your deposit needs to be ready at that point.

Deposits are often paid in two parts, making up to the 20%:

a. On the date your offer becomes unconditional (typically 10%)

b. On the date of settlement (typically the remaining 10% to make up your total deposit)

- Your home loan

The rest of the house price is covered by a loan from the bank. The bigger your deposit, the less you’ll need to borrow.

You’ll pay back your loan (plus interest) over an agreed loan term, and the bank will look at your income and expenses to determine how much you can afford to borrow.

An example of how you could get a $100,000 deposit together:

Savings: $30,000

KiwiSaver: $60,000

Gift: $10,000

Check out our calculators to understand how much you could potentially borrow based on a 20% deposit and what your home loan repayments could be based on your current numbers.

Note: Your cash savings can be made up of savings and term deposits held with banks or financial institutions.

If you have shares, investments or bonds, these often cannot be included in your total deposit amount unless they are sold and the proceeds contributed as part of your property purchase.

How to build up your personal savings for your deposit

Regularly saving (i.e. saving a portion of your income each payday) is one of the best habits to build when it comes to saving towards your home deposit. Not only does it help you grow a decent deposit, but it also shows lenders that you have the discipline to manage a home loan.

Here’s four tips on how to build good saving habits:

- Track your money

Start by paying attention to where every dollar of your money goes. Just watching your spending habits can help you make better choices. Try out a budgeting spreadsheet to understand how quickly spending and saving can add up.

- Pause before you purchase

Before you buy something that isn’t a necessity, stop and ask yourself:

Do I really need this? And is it worth the price?

Taking a minute to think about your purchases can save you a lot in the long run.

- Get the most out of your savings

Make your savings work for you by saving in a high interest account so you can get the best possible return on your balance while you continue to put money aside for your deposit.

If you’re on the lookout for a saving account to help you make the most of your money, check out our dosh strive saving account. With a strive savings account, you can:

- Earn a high interest rate with your savings on-call

- Take advantage of unlimited withdrawals so you can use your money as soon as you need to in the home buying process

- Enjoy zero account fees, minimum deposits, penalties or lock ins

- Set goals and track your progress towards your home deposit

- Funds held in dosh are DCS protected up to $100,000

4. Review your expenses on a regular basis

- Can you find a better deal for power or broadband?

- Still using that gym membership?

- Could you get better deals by looking at other options?

5. Make voluntary KiwiSaver contributions

KiwiSaver is a great way to have savings deducted from your pay without being able to touch it. If you have money available that you don't want to be tempted to spend, you can make additional payments whenever you want too. Just remember that you won’t be able to withdraw these funds until you’re purchasing your home.

Using your KiwiSaver

Your KiwiSaver can be used to help you get to your deposit sooner. You just need to be buying your first home and meet the eligibility criteria for using your KiwiSaver towards your first home.

See here for more information or check with your KiwiSaver to see if you’re eligible to withdraw.

How much can you take out?

If you meet the criteria, you can apply to withdraw almost everything in your KiwiSaver. You’ll just need to leave behind:

- $1,000 in your KiwiSaver account

- Any money that’s been transferred from an Australian super fund

What do you need to do?

When you’re applying for a home loan pre-approval, you’ll usually be asked for a KiwiSaver First Home Withdrawal Eligibility Letter. This confirms:

- That you’re eligible to withdraw funds, and

- How much you’re likely to be able to withdraw

You can get this letter (and the application form) from your KiwiSaver provider.

When can you use your KiwiSaver funds?

Once you’ve found a home or section you want to buy, it’s smart to apply for your withdrawal early as it takes time to process, and you’ll want your funds ready when you need them.

You may be able to use your KiwiSaver in two ways:

- For the deposit (while your Sale and Purchase Agreement is still conditional, usually around 10% of the purchase price)

- At settlement (once your offer goes unconditional, you can use it towards the final payment on the settlement date)

Here’s a simple checklist to help you through it:

- Talk to your solicitor – they can help guide you through the process

- Take the application to your solicitor – they can help you complete the form and make sure you have all the required documents

- Check the timeframes with your KiwiSaver provider – withdrawals can take time to process and can differ across providers - typically 10-15 working days

Getting your accounts ready to apply

When applying for a home loan, banks will assess a few things to determine whether you can meet your new home loan repayments. They take into consideration whether:

- You maintain a positive account balance

- Your expenses are reasonable

- Your current level of loan repayments (personal loan or credit cards) can be well covered by your income

- You make your regular payments on time every time

Here are 5 tips to get your personal finances home loan ready:

- Review and keep track of your expenses such as food, eating out and subscriptions. Try cut back of unnecessary expenses if you can. You can still enjoy life; however, it does help to cut back. Having a budget can help you stay on top of your expenses.

- Keep your transactional accounts in a positive balance. Avoid going into unarranged overdraft.

- Scheduling your bills around your pay or putting money aside for bills when you get paid is a good way to show you are good at making scheduled payments. Set them up as an AP, this way you'll never miss a payment.

- Limit your use of Buy Now Pay Later. If you do need to use them ensure you pay them off on time.

- If you have credit cards or other loans, be conscious of the balance and limits. Using a credit card and paying it off is fine but your credit card repayments will be considered in your ability to make home loan repayments. Can you reduce your limits or reduce the number of credit cards you have? If you have multiple cards, focus on paying down one and then closing it.

A good way to think of it is how much money do you have left over from your pay once you have paid your expenses, rent, existing loan repayments and other commitments and can you increase this amount?

How much can you afford

Once you have your deposit sorted. It’s time to tackle the next part: finding out the amount a lender is willing to lend to you.

When you apply for a home loan, the lender will take a detailed look at your money habits. It’s not just about how much you earn; it’s about how well you manage what comes in and what goes out.

Lenders want to be confident that you can comfortably afford your repayments, even if interest rates rise. The goal? A home loan that sets you up for success, not stress.

What are lenders typically looking at with your finances?

- How much can you realistically afford to pay?

- Any changes expected in your income or expenses over the next year?

- Are you managing your money well or juggling high-interest repayments?

- How many dependents do you support?

- Could you still make repayments if interest rates increase?

- Are you likely to stay committed to your loan long-term?

Want to improve your “lendability”?

The more financially fit you are, the easier it’ll be to get approved and potentially for a higher amount. Here are some practical ways to boost your financial position before applying for a home loan:

Save regularly: Showing a consistent savings habit tells the lender you’re ready for the commitment of a home loan

Clear high-interest debt: Try to pay off any debts such as Buy Now Pay Later, personal loans and hire purchases.

Cut back on credit cards: Fewer credit cards and lower limits can boost your borrowing power. Even if you pay them off, having a credit card limit will reduce how much you can borrow. Consider replacing your credit cards with debit cards, this helps paint a clearer picture of your spending without the impact of using credit

Maintain good account history: Make sure you pay bills and debts on time and try avoiding going into unarranged overdraft. Strong account conduct shows lenders that you’re reliable and likely to meet your loan obligations.

Trim the extras: Subscriptions and small outgoings add up. It might be time to review the Netflix subscription and weekend splurges.

Should I borrow less?

Just because you can borrow a big chuck of money doesn’t mean you should. A more modest loan might leave you with more breathing room in your budget – for things like travel, emergencies or future life changes.

Owning a home should feel empowering, not overwhelming. So, weigh up your priorities, think long-term.

The costs of buying and owning a home in New Zealand

It’s important to understand the costs involved with buying and owning a home in NZ. Here are costs you’ll need to consider which you may want to start saving for while you save for your deposit.

Professionals you’ll need to consult

During the home buying process, you’ll need to consult a few professionals to help you along the way.

A Solicitor/lawyer:

Buying a home comes with a bit of legal fine print, so it’s important to engage a solicitor early on. Ideally before you make an offer or bid at auction. They’ll handle the legal side of things, making sure everything’s in check and that you’re protected throughout the process. Legal fees can vary, so it’s worth requesting estimates before choosing who to work with.

Building inspector:

A building inspector helps you understand what’s really going on behind the walls of a home. They’ll check the condition of the property and let you know if there are any issues – big or small – that could affect your decision. It’s a smart move before you commit, especially for peace of mind.

Family and friends:

Your home buying journey isn’t something you have to do alone. While your family and friends may not be ‘professionals’, people that you trust can be a huge support, especially if they have bought a property themselves before. They may be able to give you honest feedback on properties you’re considering or just celebrate with you when you finally get the keys.

Financial advisor:

Before making any big financial decisions, it’s best practice to check in with a financial advisor to help you make the best decision for your financial situation.

Getting pre-approval: what it means and why it matters

Getting pre-approval means the bank has agreed to lend you up to a certain amount, if you meet the conditions outlined in the approval.

Having pre-approval can make the process a lot smoother as:

- It gives you a clear spending limit so you can search for a house with confidence

- It shows real estate agents and sellers that you’re serious, which can help you stand out in a competitive market

Tip: If you’re planning to bid at auction, you’ll need full approval in place before you go ahead. So, make sure to select the ‘I have found a property to buy’ option if applying for a home loan with dosh.

What’s the difference between pre-approval and full approval?

Pre-approval is basically saying:

“Yes. As long as you choose a home that ticks the right boxes, we will support your purchase.”

Pre-approval gives you a clear idea of how much you might be able to borrow. It’s super helpful when you’re starting your house search, but it’s not a guarantee just yet.

Your lender will still need to review the property you want to buy before they can give you the final green light. The house must meet a few conditions (like type, location, and value), and in some cases, extra conditions may apply based on your situation.

With pre-approval you can:

- Search for properties with a budget in mind

- Make conditional offers (check with your solicitor on the conditions to include in your offer)

Full approval means your lender has reviewed the details of the exact home you’re planning to buy, and everything checks out.

With full approval, you’re in a strong position to:

- Make an offer on your chosen property with confidence

- Bid at auction, knowing your finances are sorted

Hot tip: Start thinking about insurance at this stage.

Once you get further down the buying process with looking to put an offer on a specific house, your lender is likely to ask you to sort home insurance as a condition to your finances. While you start your property search, start researching insurance companies so you can be extra prepared.

2. Searching for your new home

After sorting your deposit, pre-approval and home loan team, you’re ready to start searching for your new home.

Here’s some insight that can help you with your search.

Understand the different property types available

Types of land ownership in New Zealand:

In New Zealand, the most common know land ownership types are:

Freehold: The most common and straightforward type of property ownership in New Zealand. You own the land and the house on it outright. You are in control of the entire property (within council rules) and comes with the most flexibility.

Leasehold: With leasehold properties, you own the house, but not the land it sits on. Instead, you lease the land from the landowner, and you pay ground rent for the land. Leasehold properties are often cheaper upfront, but the ground rent can increase and impact on your long-term budget.

Cross-lease: With a cross-lease property, you own a share of the land with others (often seen in a small group of flats or townhouses) and lease your individual unit from all the co-owners. You’ll usually need agreement from the other owners to make big changes to your home (e.g. building an extension or renovating the exterior).

Unit titles: Unit titles are common in apartments or townhouse complexes. You own your individual unit, but you share ownership of common areas (like driveways or gardens) through a body corporate. The body corporate will set rules and regular fees for upkeep and maintenance.

Each landownership type comes with its own features and considerations so it’s best to talk to your solicitor and understand what each type could mean for you and your situation.

Understand the different building types available

The most building types you’ll come across in New Zealand:

- Existing houses – generally the simplest building type to purchase and be approved for a home loan

- Apartments and terrace houses – If you purchase these types of building, you may become a shared owner of common area of the property (e.g. you may become a member of the body corporate which may include extra costs and responsibilities.

- Building or buying off the plans – This can be a good option to buy your ideal property however, this can come with additional things to consider, and it is worth talking to a professional about this option. Note, construction loans are currently not available with dosh.

Creating your ideal home checklist

Deciding on a home to buy is a big commitment so it’s best to do plenty of research and get specific on the property features that are important to you. Before you start your search, create your own home buying checklist so you can search in confidence and don’t waste your time looking at properties that aren’t suitable for you.

It can be helpful to break down your ideal property features into categories of wants and needs- as you may need to make some compromises.

Criteria you may want to consider including in your home buying checklist:

Location:

- Proximity to city centre or public transport

- Within school zones

- Low crime rate

- Nearby to amenities and employment opportunities

Type of house:

- A home that’s ready to move into without the need for renovations

- Number of bathrooms and bedrooms required

- Energy efficiency

- Layout of the land/home

- Has a garage

Section:

- Enough land for your needs

- Large garden space or outdoor living space

- Low maintenance garden

Once you’ve found a property that meets your criteria, it’s worth doing a few checks before going to the offer stage.

- Does it get good sunlight? Try visiting at different times of the day to see how much natural light it gets.

- What’s the neighbourhood like? Take a walk around and check out how you feel in the neighbourhood.

- Is it close to amenities you need? Shops, public transport, schools, parks being close by can make life easier.

- Is it warm and dry? Check for insulation and heating.

- What’s the general condition like? Keep an eye on the roof, exterior, and outdoor spaces. Any red flags or future costs to consider?

- Are there any unconsented works? Make sure all renovations or additions are council approved.

- Is it insurable? Some properties can be tricky to insure – worth checking this early.

When purchasing your first home, it can be difficult to find a property that meets all of your requirements within the budget your lender has pre-approved you for.

Different types of offers and ways the house will be sold

When buying a home in New Zealand, there are a few ways a house can be sold.

The buying process can be done via:

- Negotiation

- Auction

- Tender

- Deadline sale

- Fixed price/asking price

Here’s a breakdown on what they mean:

Negotiation: This is a more flexible option and less time restrictive. You make an offer (with or without conditions), and the seller can accept, decline or counteroffer. There is often room to talk and tweak the deal.

This is a great way of buying if you want to include conditions like a building inspection or finance approval. However, with negotiation there is little transparency around the seller's expectations on sale price, which means you may need to rely on the Real Estate agent for guidance.

Auction: This is a fast-paced, competitive way to buy a home. An auction requires you to show up on auction day and bid against other buyers. If you win the auction, the sale is unconditional (so it’s important to have all your checks and finances on the property sorted before going to the auction). If you are successful in winning the auction, you have bought the property, and a 10% deposit is required to be paid on the day.

Tip: Make sure you’ve got full loan approval on the property, and your lawyer has reviewed the Sale and Purchase Agreement before auction day.

Tender: Buying by tender requires you to submit your best offer in writing, without knowing what any other buyers are offering. The seller picks the offer they like best. Any offers they don’t pick will be declined and there’s often not a second chance so it’s best to put your best offer in.

Tip: Your offer can include conditions, but due to the competitive nature it's best to get advice from your lawyer before submitting your offer so figure out what your best offer can be.

Deadline sale: This is like a tender, but a bit more open. There will be a set deadline to have all offers in, but the seller can accept an offer at any time, even before the deadline. That means if you find a home you love on deadline sale, don’t wait too long. Offers can be conditional or unconditional. You may come up against other offers, so make your best offer.

Fixed price/asking price: This is the most straightforward option. The seller lists a price, and you can decide to offer that price, less or more. There’s room to negotiate and you can include conditions.

This is the ideal situation for buying as a first home buyer as you know the price the seller wants and you have a chance to do all the checks, sort your conditions before committing and negotiate.

When you’re ready to make an offer, there are two options: conditional and unconditional

Conditional offer: A conditional offer means you are ready to purchase the house, if certain conditions are met first. You can include conditions in your offer that need to be met before the Sale Purchase agreement becomes unconditional. Each condition comes with a deadline, and every condition needs to be met by that date. If all your conditions are met your Solicitor will confirm your offer as being unconditional.

Common conditions include:

- Getting a satisfactory building inspection report

- Confirming your finance (aka getting your lenders full approval for you to get a home loan on the property)

- Reviewing the LIM report from the local council

- Solicitor’s approval, allowing your solicitor an opportunity to end your agreement if they find something about the property that isn’t right

Unconditional offer: An unconditional offer means you’re all in, no conditions, no backing out. Once the seller accepts, you’re legally committed to going through with the purchase. That is why it’s super important to do your due diligence upfront. Unconditional offers can be powerful, especially in competitive markets but only if you’re totally ready. Make sure to talk it through with your solicitor before making your offer.

Before you make your unconditional offer, make sure you have:

- Reviewed the LIM report

- Had a building inspection if needed

- Confirmed your full home loan approval

- Got your solicitor to check over the Sale and Purchase Agreement

Either way you make your offer, you should always have your solicitor check any Sale and Purchase Agreements before you go ahead.

Property reports to consider

Before you go ahead with buying a property, these reports can help you spot red flags, avoid surprise costs later down the track and help you feel more confident about your decision.

LIM report (Land Information Memorandum): A council report showing everything the local council knows about the property. It can reveal zoning, consents, potential hazards (like flood risks) and more. You can order the LIM report from the local council or ask your lawyer to help.

Building inspection report: A qualified building inspector will check on the condition of the house. It can uncover structural issues, leaks or hidden damage that could cost you later.

Property title/record of Title: A legal document detailing who owns the property and any rights, restrictions or shared access. This helps you understand exactly what you’re buying (especially for cross-lease or unit titles). Typically, your solicitor will get this for you.

Valuation report: An independent valuation of the property’s market value. Some lenders may request one in certain situations to confirm the market value of a property before they approve the loan.

What your solicitor will do in the process

As buying a home comes with contracts and legal terms, a solicitor will be your legal guide who makes sure everything is above board and protects your interests throughout the process.

Here’s what they’ll help with:

- Ensuring the Sale and Purchase Agreement is fair, and you understand what you’re agreeing to. They can also help you add conditions (such as a building inspection or subject to finance) if needed.

- Checking the property title and looking for any restrictions, shared driveways or easements that you should be aware of.

- Helping with KiwiSaver. If you are using your KiwiSaver towards your deposit, your solicitor will help you get the paperwork sorted and make sure the money is ready in time.

- Managing the money on settlement day. They’ll make sure the funds are transferred to the seller and that the property officially becomes yours.

- Liaising with your bank and the seller’s lawyer. They’ll handle the back and forth between your lender and the seller’s legal team to make sure everything happens smoothly.

- The Ownership transfer of the property from a seller to a buyer, they will guide you through the process of signing loan documentation and finalising the property transfer and mortgage registration with Land Information NZ (LINZ) on settlement day.

Ready to apply for full loan approval?

Before your offer becomes unconditional, you’ll need to apply for loan approval on the property you’re wanting to purchase.

If you have pre-approval already sorted, all you’ll need to do is send the draft Sale and purchase agreement to your lender, along with any other supporting documentation you may have on it. This is where your bank will assess the property you want to buy before providing you with full approval. In some cases, the bank may require a property valuation and or proof of house insurance.

3. From offer to settlement

Once you have made your offer and gone unconditional on a property, it’s time to start looking towards settlement day. Here’s what to expect in the lead up so everything is in line for the property to become yours.

Pre-settlement tasks to tick off

Before your settlement day arrives, there are a few things to consider.

Insurance: Before settlement day, you’ll need to have home insurance in place if you haven’t already been asked by your lender.

KiwiSaver: If you’re using KiwiSaver towards your deposit and haven’t already submitted your withdrawal application, now is the time to do so. Make sure to check with your provider on how long it will take to process the withdrawal. (refer to KiwiSaver section)

Final inspections: Before settlement day, arrange to complete a pre-settlement inspection with the real estate agent. In this inspection, you can make sure that any inclusions in the Sale and Purchase Agreement are carried out. You’ll also want to check that everything on the property is in working order (e.g. appliances, lights, heat pumps etc.) and there has been no damage since the Sale and Purchase Agreement was signed.

Remaining funds: Make sure you have transferred any remaining funds to cover the outstanding balance of your deposit. Your solicitor will let you know when and where the funds need to go. And don’t forget to check your transfer limit if you are sending the funds via bank transfer.

Get your utilities ready to go: Start researching power and internet companies so you can have them set up to be ready to go or switched over on your settlement date.

What happens on settlement day?

Settlement day is an exciting milestone in your home buying journey. This is the day the property title is transferred to you. Your solicitor will handle most of the work but here’s what happens on settlement day:

- Your funds will be transferred from your lawyer to the seller’s lawyer.

- The property title is transferred to your name, so you officially become the legal owner of the property.

- You get the keys. 🎉 Once everything has been confirmed by both your lawyer and the seller’s lawyer, you’ll be notified on when and where you can collect your keys.

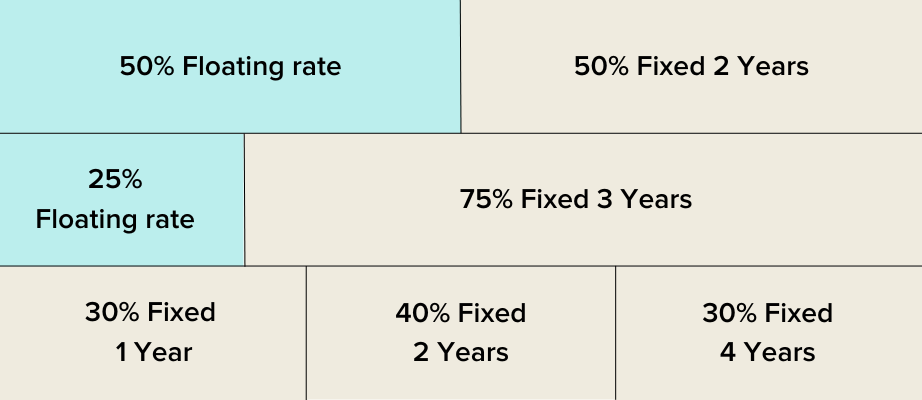

Ways you can structure your loan

There are a few ways you can choose to split your loan to suit your financial situation. Check in with your financial advisor about the best way to structure your home loan.

Reasons you may consider splitting your loan:

- Helps spread risk across multiple loan periods if interest rates go up or down.

- Have certainty that repayments on your fixed portion will stay the same for the chosen period.

- Utilise the flexibility of a floating rate and be able to pay off the floating portion as fast as you like.

Here are some examples of a loan being split:

Paying off your loan faster

Typically, a home loan can take up to 30 years to pay off if you choose to go with the lowest repayment option. However, paying off your home loan faster can save you money and opens up freedom for you later down the track.

Benefits to paying off your home loan early:

- Save on interest as the earlier you pay off your loan, the less interest you’ll pay overall.

- Less financial stress later as you won’t have to worry about paying off your home loan and owning your home outright can give you peace of mind.

- Paying off your home loan faster increases the equity you have in it, which can be helpful if you want to renovate, refinance or borrow against it in the future.

- The smaller your loan, the less affected by interest rates you’ll be if they increase.

- The quicker you pay off your loan, the sooner you can consider using that money for other things such as travel, investments or retirement.

Ways you can pay off your home loan faster:

Make extra repayments when you can:

- Even small payments can chip away at your loan and reduce the interest you pay overtime.

Switch to fortnightly payments instead of monthly:

- Fortnightly repayments mean you pay the equivalent to one extra month’s repayments each year.

Increase your repayments:

- If you get a pay rise or reduce your expenses, consider putting a bit more toward your loan each pay cycle. Tip: If you’re on a fixed interest rate, you can ask your lender if you can increase your repayments when you refix.

Put lump sums towards your home loan:

- If you receive a bonus, tax refund or some savings, consider putting it into your home loan. A one-off lump sum goes straight toward reducing your loan balance, meaning less interest.

If you are interested in paying off your loan faster, make sure to first check with your lender as some fixed home loans have limits/restrictions on extra repayments. There may also be the possibility of having to pay a pre-payment fee aka break fee, if your loan is on a fixed rate at the time you want to make a lump sum payment. The best time to investigate paying off your loan faster is at the time of your fixed interest expiry date.

Disclaimer:

Dosh Home Loans are approved, issued and managed by Westpac New Zealand Limited and promoted by Dosh. Lending and eligibility criteria and terms and conditions apply.

This guide is for information purposes only. Dosh does not provide any financial advice or recommendations. Any information we make available to you does not take into account your particular investment objectives, financial situation, or investment needs. None of the information we provide can be taken as investment, financial, or tax advice.

The information in this guide is current as of October 2025 and may vary from time to time.

.png)

.png)

.png)

Dosh is not a registered bank. However, your funds are held at a NZ registered bank.